English

English

Bloomreach Commerce Pulse: February’s Data Indicates Consumers Buckling Down Due to Economic Pressure and Global Uncertainty

By Brian Walker

03/22/2022

Our Bloomreach Commerce Pulse monthly articles explore the most interesting Bloomreach Commerce Pulse results and provide key insights for ecommerce professionals and industry observers looking to benchmark and understand what is happening in the market. They reveal current trends and help businesses fully understand the digital commerce marketplace.

When we look at the industry numbers for February 2022, the first impression that immediately comes to the surface is that inflation is very much at the forefront of people’s minds right now — both in the US and across the globe. All of the sociopolitical world events unfolding simultaneously around us are very much dictating how people are choosing to spend their money and where exactly they’re allocating it.

Lately, we’ve been taking a look at The University of Michigan’s Surveys of Consumers before delving into our own data, so let’s continue that trend. According to the preliminary survey insights for February, it looks like consumer sentiment continues to decline, which chief economist Richard Curtin attributes to a combination of inflation and the decrease in inflation-adjusted incomes. Unfortunately, the devastating events in Ukraine and rising fuel prices are not helping the pressure consumers feel now and have experienced throughout the pandemic.

Similar to Bloomreach’s January 2022 Commerce Pulse data, we’re continuing to see a downward trend in site traffic month-over-month (MoM) and year-over-year (YoY) across many segments. Looking specifically at geographies, traffic in North America was down 14.3% since January 2022 and nearly 16% since February of last year. In the United Kingdom and Europe, the decrease in MoM traffic looked about the same as in North America, yet the YoY numbers are even more jarring with a decline of approximately 19%.

The increase in average order size (AOS) continues to rise in North America, however, with a lift of 2.8% MoM and almost 12% YoY. Europe and the UK’s numbers succeed even with these impressive boosts: average order size (AOS) reached a 7.7% MoM lift and an astounding 27.9% YoY increase. These changes are dramatic, to say the least. So, what are the numbers telling us as Q1 2022 rapidly comes to a close? Here are the key takeaway points from February 2022, according to our Bloomreach Commerce Pulse data.

Inflation Won’t Get Better Before It Gets Worse

First things first, we see a continuing theme in February that has stuck out to many economic analysts and experts throughout the pandemic: Even though the stock market continues to perform well, the general populace is feeling the weight of the pandemic, and the disconnect between Wall Street and Main Street has never felt so obvious. That’s why online traffic and sales continue to decline in most of the categories that we analyzed. Online sales are also down MoM across the board, with a significant 24.7% plunge in North America and a 4% drop in the UK and Europe — plus, a nearly equivalent decrease of 14% YoY in all three geographies.

The decline in traffic and sales likely points to strict consumer discretion in spending due to inflation and the global environment customers are now operating within. The larger order values we’re seeing across geographical regions (an 8.9% increase YoY in North America, for example) only imply that the prices of the items being purchased are higher than they were the year prior. Since consumer attention has shifted to larger existential matters, it’s ultimately changing the way consumers feel about spending money right now.

Grocery Continues to Track Positively, Indicating a Long-term Pivot

Despite all the economic uncertainty, certain verticals, like grocery, continue to stay stable even as the pandemic moves to a different phase. Like apparel, home furnishings, and luxury, grocery is up in AOS because of inflation — by 10%, to be exact. Unlike most of our segments, grocery is also rising in both traffic (+10.6%) and sales (+2%) YoY. Even though groceries are considered a necessity, it doesn’t necessarily explain the steadiness in its numbers, especially since we’re also seeing luxury take a serious upward turn in sales by an incredible 38.5% YoY.

Based on our findings, the stability in grocery’s traffic and sales numbers solidifies its lasting adoption in ecommerce. This shift is happening for several reasons. Not only are people changing the frequency of times they shop in-store per month, but they also purchase food and other necessities — online and otherwise — with supply chain disruptions in mind. For decades, grocery stores had a reputation, especially in the US, for their vast amount of stock and eclectic brand representation. Now, shoppers are more impulsive in buying certain items when they become available.

Luxury Makes a Victorious Return

Since the end of 2021, luxury continues to make a significant rebound, which we mentioned earlier was +38.5% in traffic and +48.9% in sales YoY. With the pandemic easing, there is a rush to revamp static closets gathering stay-at-home mothballs. Yet, this rush to luxury retail brands is happening among a select population of well-to-do consumers, whose overall incomes and spending power have increased. This assertion is illustrated by the 11% lift in AOS MoM and nearly 5% bump YoY. Clearly, the data demonstrates an economic imbalance occurring in real time.

As the world slowly but surely reemerges into public spaces, people are attending important occasions, like weddings, and picking up travel again, so luxury sales are responding accordingly. Consumers want (and need) new clothes, shoes, bags, and so forth to participate in these endeavors, and their preferences are being reflected in the numbers we are seeing. With all the green lights in this category, we don’t see the rush to luxury goods slowing down any time soon.

Home Furnishing and Improvement Drop, But It’s Not What You Think

Another shift that stood out to us was the drop in home furnishing traffic by 49% YoY. Similarly, home improvement traffic is down by 31.6% YoY, and sales declined in improvement by a substantial 44% YoY. Like many of our other segments, AOS increased in both furnishing and improvement by 27.4% and 18.4% YoY, respectively. Again, we are seeing fewer shoppers, but certain customers are making larger purchases at a higher rate. This trend can most likely be associated with all the new homebuyers in the market, as opposed to the general population nesting at home.

These declines, along with the 21.8% drop in monthly home furnishing sales, could also be connected to natural disasters and a failure to meet demand. Several countries that are large furnishing manufacturers were battling various natural disasters in February. For example, Japan was dealing with ash and smoke spew after a volcanic eruption of Mt. Shindake, while those in the UK and central Europe were facing the harsh winds and rain of Storms Dennis and Ciara. As climate events continue to worsen due to global warming, these supply chain issues are worth keeping a close eye on.

Say Goodbye to Pandemic-based Keywords…For Now

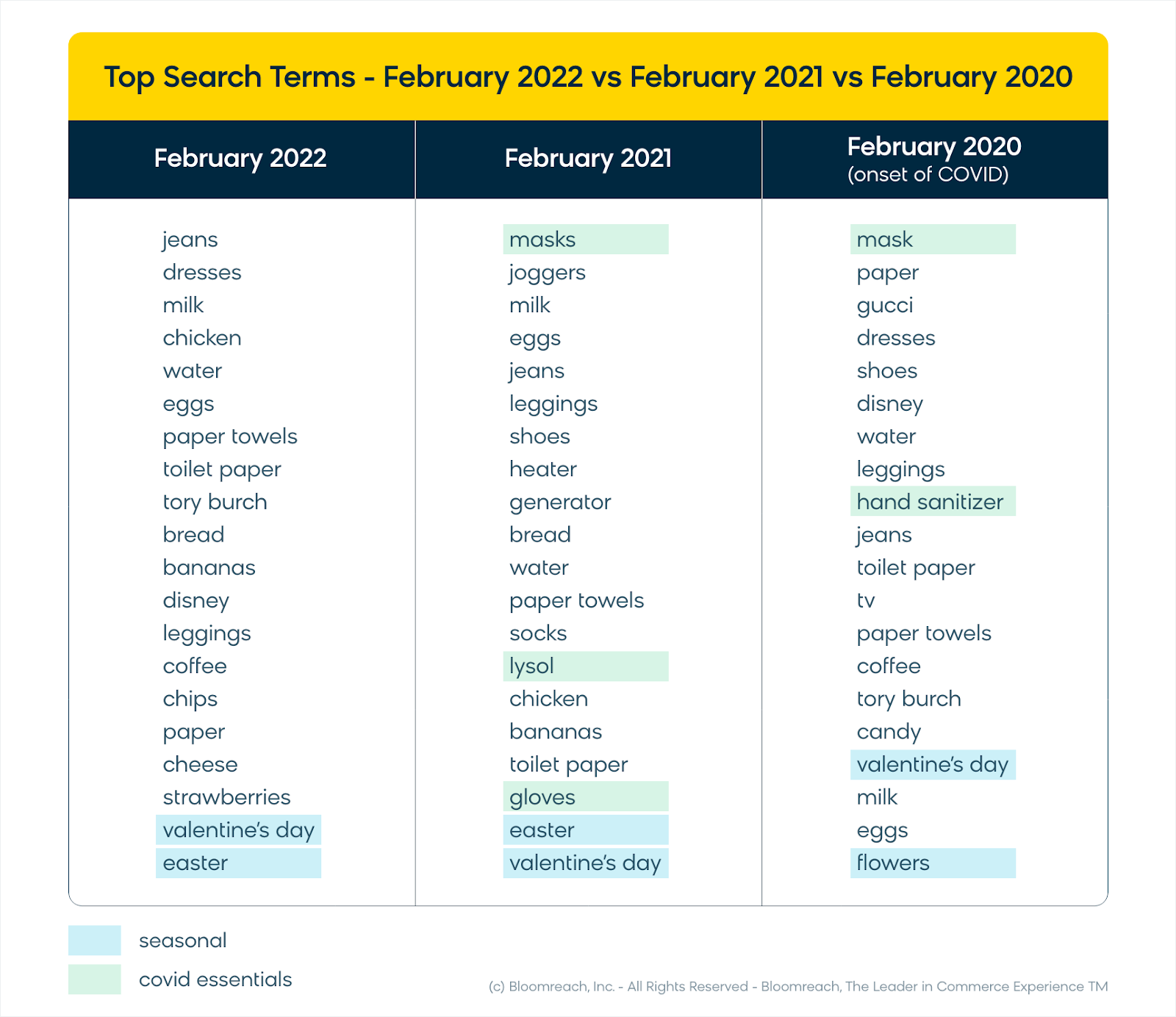

Finally, popular search terms always give us a solid understanding of shoppers’ intent across the globe. This month, searchers were looking for a lot of their ordinary staples, including “water,” “bread,” “eggs,” “paper towels,” and “toilet paper.” Upcoming holidays, like “Valentine’s Day” and “Easter,” were also represented in the mix.

However, we did notice some significant changes in search terms from February 2021 to February 2022. As you can see from the chart below, pandemic search terms, such as “masks,” “Lysol,” and “gloves” have completely disappeared from users’ search queries, even with the Omicron variant. Brand searches, which were not represented at all in February 2021 search terms, also made a comeback (i.e., Disney and Tory Burch).

Interested in More Insights and Trends?

Join us for our next Commerce Pulse Quarterly roundtable to discover the shifts in consumer behavior and purchase patterns in digital commerce. Register for the virtual event here.

About Bloomreach

Bloomreach is the world’s #1 Commerce Experience Cloud, empowering brands to deliver customer journeys so personalized, they feel like magic. It offers a suite of products that drive true personalization and digital commerce growth, including: Discovery, offering AI-driven search and merchandising; Content, offering a headless CMS; and Engagement, offering a leading CDP and marketing automation solutions. Together, these solutions combine the power of unified customer and product data with the speed and scale of AI-optimization, enabling revenue-driving digital commerce experiences that convert on any channel and every journey. Bloomreach serves over 850 global brands including Albertsons, Bosch, Puma, FC Bayern München, and Marks & Spencer.

Found this useful? Subscribe to our newsletter or share it.

Brian Walker

Strategy Consultant and Former CSO at Bloomreach

Brian Walker is a veteran commerce strategy and marketing leader focused on the transformation of digital customer engagement and commerce.

He has held a wide range of roles across the commerce landscape - from practitioner to analyst to consultant to software strategy and marketing leader - giving him a unique view on the evolving capabilities and approaches necessary for businesses to thrive as digital channels have evolved to become the primary driver for business growth.

![]()